Moving your retirement savings between 401k plans is a pain. It often means you must make two separate distribution transactions and be hit with tax consequences. But, with the Advancing Auto-Portability Act of 2022, things can get a lot easier.

A lower wage and a high employee turnover rate can make auto-portability especially useful in industries like retail and transportation, where accounts with balances under $5,000 are automatically rolled into IRAs. SECURE 2.0 proposals could increase involuntary cash-out thresholds to $7,000, thereby expanding potential prospects for auto-portability product markets.

Here is everything you need to know about how auto-portability changes the retirement industry landscape. So, let’s get started.

Auto-portability

Auto-portability is a feature of financial technology in the retirement service segment that allows for the seamless transfer of retirement savings from one plan to another. Auto-portability ensures that retirement savings are preserved when an individual changes jobs and that they can continue to grow their retirement nest egg without starting from scratch each time they change employers. This is a critical feature for those who may change jobs frequently or are otherwise unable to stay with the same employer for the duration of their career.

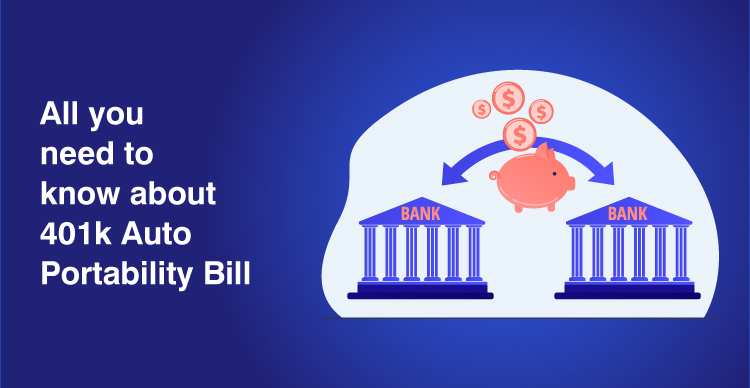

How does Auto-portability work?

Retirement plan portability starts by “locating” retirement account information for moved participants. This is done by matching the participant’s Social Security number with information from the National Change of Address (NCOA) database. Once the account information has been located, the technology “matches” the information with the correct new employer; this is done by comparing the information in the participant’s account with data from the Employer Identification Number (EIN) database. Finally, the auto-portability software “transfers” the account information to the new employer. This is done by sending a file to the new employer that contains the account information.

When an individual opens a new 401(k) account, their previous employer’s IRA is automatically rolled over to the new employer’s plan. This is done to keep the individual’s retirement savings in one place. With auto-portability, your plan can skip the default IRA phase and go straight to your new employer’s plan. This way, you won’t have to worry about establishing a new account and transferring your savings. Participants must provide consent when their default IRA balance matches a new employer plan account balance. The default roll-in happens if no consent is given within 30 days.

What problems does it solve?

Problem 1 – Cash out leakage –

Do you know that 14.8 million job transitions happen yearly, of which 6 million people completely cash out their retirement savings? Why?

The inconvenience of transferring retirement plans,

Time required to process even a small amount of transfer, and

Having doubts about the security of retirement funds.

With auto-portability, low-balance IRAs are moved into employer-sponsored plans, which can be consolidated with future savings.

Problem 2 – Duplicate Accounts & Associated Costs:

Needless to say, the duplication and the costs incurred in maintaining them every time an employee transfers their retirement savings account.

By automating the transfer of savings, employers can reduce unnecessary expenses associated with maintaining multiple accounts.

Problem 3 – Missing Participants

A gradual erosion of low-balance IRA account balances, coupled with anemic money market returns and default accounts with missing participants.

Participant’s retirement savings are less likely to be classified as “lost or missing” when they consolidate their current-employer plans.

How can it help a plan sponsor?

A plan sponsor can connect with auto-portability services in a few different ways. The first is by working with their current recordkeeper or administrator. Often, these firms will have a relationship with an auto-portability service provider and can help facilitate the transition for the plan sponsor.

The second way a plan sponsor can connect with an auto-portability service is by working with their financial advisor. Advisors who are familiar with the process can help connect the sponsor with the right service provider and ensure a smooth transition.

Finally, the sponsor can reach out to the service providers directly to learn more about their offerings and how to get started.

What a plan participant needs to know about auto-portability?

As the auto-portability landscape continues to evolve, it’s important for plan participants to stay up-to-date on the latest developments. Here are a few things to keep in mind:

1. The rules and regulations governing auto-portability are still being finalized, so there may be changes in the future.

2. Not all 401(k) providers offer auto-portability, so it’s important to check with your provider to see if they offer this option.

3. Auto-portability may not be right for everyone. If you’re happy with your current 401(k) provider and don’t want to switch, there’s no need to do so.

4. There may be fees associated with auto-portability, so be sure to ask your provider about any potential charges.

By staying informed about auto-portability, you can make sure that you’re making the best decision for your retirement savings.

Conclusion

Finally, auto-portability increases security across the US retirement plan industry with no paperwork or time spent on the process by the employees. This reduces stress for the employee for the new employer to manage retirement assets. Plan sponsors are quickly adopting it to provide plan participants with ease and security. The industry can reach new heights with advances like these. However, updating the legacy record keeping software to accommodate the ever-changing policies, rules, and regulations can be frustrating. That is why we have architected our CORE suite of solutions so that the business rules sit separately from the code. Adapting to the newer rules and regulations is easier this way. Interested to know more? Contact today!